The federal government and 42 states impose a tax on capital gains, most as part of their income tax. While widespread, taxes on capital gains are an unstable revenue source, with receipts rising sharply in booms and falling deeply in recessions. Capital gains tax increases and cuts have clear incentive effects, with high rates incentivizing investors to hold onto assets that have appreciated in value rather than selling them and investing the profit elsewhere (known as the “lock-in” effect). Taxes on capital gains are also a double tax on investing activity, often applying to fictitious income due to lack of inflation adjustment.

Capital gains are the profits earned as income from the selling of an asset. The tax is imposed on the difference between the original purchase price (“basis”) and the price when sold (“realization”). When sold at a loss, it is a capital loss. While all gains are subject to capital gains tax, the most common assets subject to the tax are stocks, bonds, cars, cryptocurrency, jewelry, farms, and art. Assets sold after a year are long-term capital gains or losses; other sales are short-term capital gains or losses. Sales of primary homes are exempt in the U.S. up to $250,000 in gain, as are unrealized gains (assets that have not yet been sold).

The federal government imposes a tax on capital gains as part of the federal income tax. The tax on long-term capital gains is at a preferential rate (15%, 20%, or 23.8% depending on income bracket).

All 41 states (plus DC) with an income tax impose it on capital gains, plus Washington has a special capital gains tax (7% on gains of $250,000 or more in a year). One state (Minnesota) has an extra tax (1%) on capital gains on top of the income tax, while another state (Montana) has a lower rate (4.1%, compared to 5.9% income tax). Six states exempt a share of capital gains from their income tax: Arizona (25%), Arkansas (50%), New Mexico (40%), North Dakota (40%), South Carolina (44%), and Wisconsin (30%). California has the highest tax on capital gains (13.3%), followed by New York (10.9%), DC and New Jersey (10.75%), and Oregon (9.9%), all on top of the federal income tax. Eight states have no tax on capital gains: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, and Wyoming.

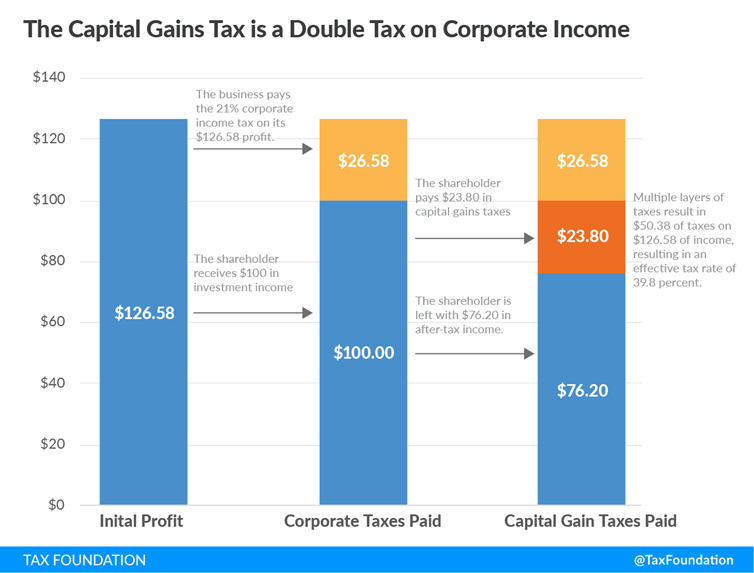

When imposed on earnings from corporate income (such as stocks or bonds), it is a second layer of tax on top of the corporate income tax, discouraging business activity. As this chart from the Tax Foundation illustrates, a 23.8% capital gains tax, when added to corporate income taxes paid on the same underlying investment, results in an effective tax rate of 39.8%.

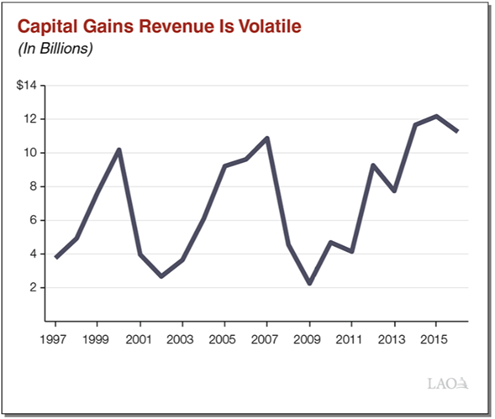

Taxes on capital gains are an unstable revenue source. Because taxes on capital gains are primarily on high-income earners with volatile incomes that rise sharply in booms and fall sharply in recessions, they magnify state budget effects. California’s Legislative Analyst Office has concluded that capital gains taxes are three times more volatile than income taxes generally and contribute to California’s budget instability. The Pew Center on the States found that capital gains are the most volatile income component, more than business income or wages. A Congressional Research Service review of federal tax data found capital gains realizations in recent years have fluctuated widely between 2% and 8.7% of gross domestic product: a yearly range between –80% and +50%.

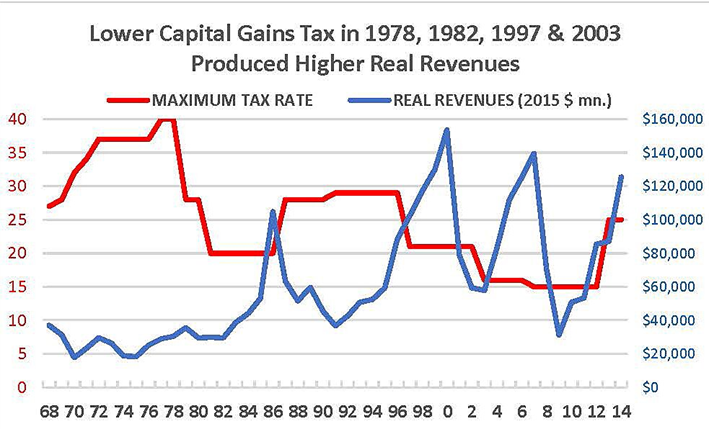

Capital gains tax increases and cuts have clear incentive effects, and high capital gains taxes cause “lock-in” that impedes mobility. Increased sales, increased income, and increased tax revenue have accompanied federal capital gains tax cuts. Capital gains tax increases are preceded by a sharp increase in revenue before the increase takes effect, and then a steep drop-off as the below chart from the Cato Institute shows. Since capital gains tax is imposed on sale, investors will sell assets less frequently if capital gains taxes are high. One-third of capital gains are business sales.

Taxes on capital gains often tax fictitious income. No inflation adjustment is made to an asset’s basis, resulting in tax being paid on what appears to be a gain but is really a loss or a smaller gain after adjusting for inflation. Adjusting federal capital gains income basis for inflation has frequently been proposed but has not been enacted.

Potential federal-level reforms include reducing capital gains income tax rates to minimize double taxation and volatility effects on federal revenue, as well as allowing taxpayers to adjust basis to account for inflation.

At the state level, states could exempt all (as 8 states do) or some (as 7 more states do) capital gains income from state income tax. States could also dedicate capital gains tax collections for one-time expenses only to mitigate volatility. At a minimum, states should ask revenue officials to study past tax collections and volatility from the tax on capital gains income.