(pdf)

On September 12, 2019, Senator Ron Wyden (D-OR), the ranking member of the Senate Finance committee, released his proposal to overhaul the taxation of capital gains. His working paper, “Treat Wealth Like Wages,” outlines the broad contours of a proposal to move the U.S. to a “mark-to-market” tax system.[1]Such a system would impose taxes on the value of an asset annually, rather than imposing tax when the asset is eventually sold.

The working paper invites stakeholders to provide comments on the proposal. While not exhaustive, this paper will outline the proposal from Senator Wyden and discuss a multitude of issues with such a system.[2]

Also known as anti-deferral accounting, mark-to-market taxation would be difficult to implement given challenges related to valuations, exemptions, transition rules, and treatment of losses, among other matters. The issues identified in this paper make it difficult, if not impossible, to imagine the creation of an administrable and fully functional mark-to-market tax system.

Theoretical Basis for Mark-to-Market Taxation

Defining an individual or a business’s income is a delicate task in economics and tax policy. The most commonly accepted approach uses the so-called Haig-Simons definition of income, named after economists Robert Haig and Henry Simons.[3]Plainly stated, under the Haig-Simons definition an individual’s income equals their consumption plus the change in their net worth. This broad definition means that an individual’s consumption over the year, plus any appreciation (or depreciation) in their assets, is equal to their income.

Theoretically, using the Haig-Simons definition of income suggests an income tax that taxes consumption as well as changes in net worth on an annual basis. Under this approach, economic gains or losses associated with ownership of an asset would be taxed when they occur.

In view of the administrative difficulties of such a tax, however, the U.S. system takes a realization approach, which delays the taxable event until the asset is sold. Realization does not precisely match economic gains or losses, but it does provide administrative simplicity, as questions about valuation, losses, and exemptions are less vexing.

Senator Wyden’s Proposal

Senator Wyden’s proposal builds upon the Haig-Simons definition of income and attempts to move the U.S. toward taxing capital appreciation on an annual basis, eliminating the current realization treatment for many investors.

The proposal includes several key components. Individuals with more than $1 million in income or $10 million in qualifying assets over a three year period would be taxed annually on the change in value of their tradable asset. In addition, Senator Wyden proposes eliminating the lower capital gains tax rate, instead taxing capital gains as ordinary income using the existing progressive rate schedule.

Wyden says that the tax hike—an estimated $2 trillion over a decade—would be dedicated to improving Social Security’s solvency.

Tax Rates

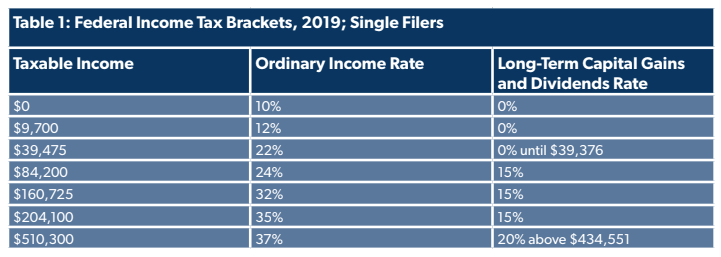

Senator Wyden’s proposal would raise the capital gains tax rate from its current 15 or 20 percent tax rate to ordinary income tax rates, which reach as high as 37 percent.[4]The proposal would also retain the net investment income tax (NIIT), which assesses an additional marginal tax rate of 3.8 percent, bringing the highest capital gains tax rate to 40.8 percent under Wyden’s proposal.

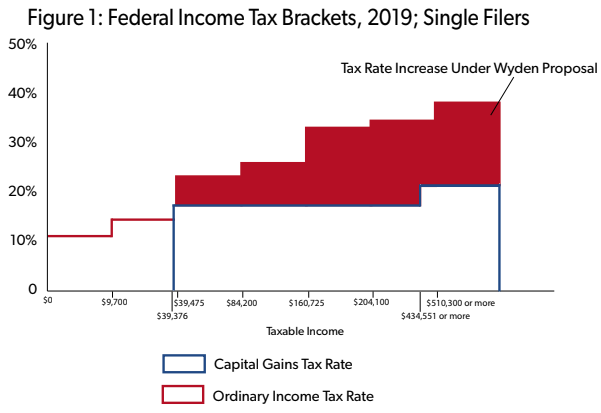

While the mark-to-market rules would only apply to the affluent, the rate increases could apply to all investors, impacting many in the middle-class. Currently, the 15 percent rate applies to any long-term gains for single filers with income levels between $39,376 and $434,550. Tying the capital gains tax to ordinary tax rates would mean that the capital gains tax burden for most investors would increase.

Under the current system, a single investor with wage income of $40,000 faces a tax rate of 15 percent on a dollar of capital income. Under Wyden’s proposal, that dollar of capital gains income would be taxed at 22 percent, a 47 percent increase. An investor with income of $84,200 who earns a dollar in capital gains income would be taxed at 24 percent, rather than 15 percent—a 60 percent increase in tax rates. Figure 1 illustrates this phenomenon.

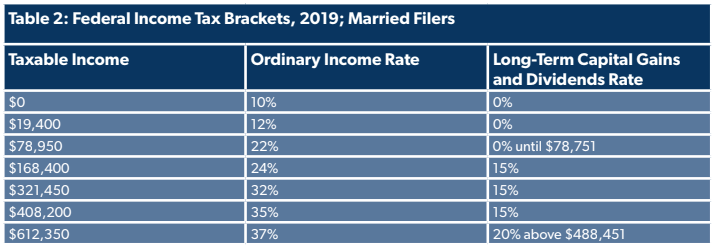

The same would apply to married filers. Married couples currently pay the 15 percent tax rate on capital gains between $78,750 to $488,850 in income. However, their 22 percent ordinary income tax rate begins at $78,950 in income, with the 24 percent bracket starting at $168,400. This means that married investors with wage income of $78,950 or more would pay more in capital gains taxes.

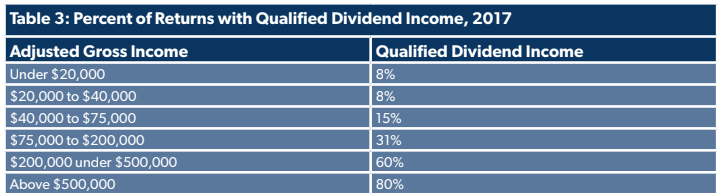

This proposal would also subject qualified dividend income to a higher rate. Qualified dividend income is generally assumed to be associated with high-income individuals, but a surprising number of low- and middle-income taxpayers have qualified dividend income, largely those close to or in retirement who use dividends as an income stream. For example, 15 percent of returns with adjusted gross income between $40,000 and $75,000 had qualified dividend income in 2017. More than 30 percent of those with adjusted gross income between $75,000 and $200,000 had qualified dividend income. Eliminating the lower rate for qualified dividends would raise taxes on these individuals.

Senator Wyden suggests that his plan could provide a middle-class safe harbor, but designing such a system could be challenging. The Senator, for example, might decide to retain the current lower rate for some investors, but make it more progressive. This would accomplish the primary goal, but would increase the number of marginal rate cliffs within the code. It would also still benefit high-income investors. Using a progressive rate structure means that some of their capital gains income would be taxed in the lower tax-rate brackets. To truly target, a credit or deduction would need to be created, but that would further increase complexity in the code.

Senator Wyden and many other proponents of higher taxes on capital make the argument that the lower tax rate on capital gains is a preference. It is true that capital gains are subject to a lower tax rate, but that is due, in part, to the double layer of tax assessed to business ownership.

Owners of corporate stock, for example, face two taxes. First, the income earned by the business is taxed at the corporate level at 21 percent. Then, what’s left over is taxed again at the individual level when it is received by a taxpayer. It is not a perfect solution, but the lower rate on capital gains does help to mitigate the impact of double taxation.

Raising tax rates to the levels imposed on ordinary income is problematic without broader integration of business income into the individual tax code.

Valuations

The key to any mark-to-market tax structure is the valuation of assets. To appropriately tax capital gains annually, the taxpayer must know the value of their assets on an annual basis. For some assets, this is relatively easy. Stock prices for publicly-traded companies are readily available, allowing both the taxpayer and the Internal Revenue Service to know its value annually. Similar arguments can be made for other easily-traded financial interests. In this way, mark-to-market taxation is analogous to our current state and local property tax structure, where owners are taxed regularly on the value of their property. This is theoretically relatively easy to value given a functioning market with ample comparable sales.

But even here, property owners often challenge their assessments, arguing the local tax assessing body misvalued the asset. Primarily due to resource constraints, states and localities do not often perform the kind of property-level analysis that would be required to produce an individual value, instead relying on spot checks, which are used to derive a county- or city-wide adjustment. This adjustment is then applied to home values across the board. This would be akin to assessing the value of stock in any publicly-traded company as having gone up 26 percent year-to-date in 2019 simply because that’s what the S&P 500 index has done, regardless of the price of the actual share in question. An individual share of stock, of course, may have moved very differently from the class of assets in which it is a part.

But not all assets are as easy to value as stocks or property. Ownership of private businesses, artwork, yachts, and other luxuries, among other assets, are difficult to appraise. These assets may have limited markets for them, or no markets at all, making valuation a guessing game. In such a scenario, naturally the incentive for a taxpayer will be to minimize the value of such assets while the incentive for revenue officials will be to maximize the value, setting up a highly-adversarial relationship that could lead to administrative difficulties from lack of independently-verifiable comparisons.

For assets that are easily-valued, the Wyden proposal suggests that the tax be based on the asset’s value on the last day of the tax year (December 31). While this is a straightforward approach, there are reasons to believe that it could lead to significant problems as investors respond by driving down the stock and bond markets on that day each year. The market is already subject to the so-called “December Effect,” as investors look to realize some losses to reduce their taxable gains for the year, exerting downward pressure on prices. This then leads to a “January Effect,” where asset prices increase. If all investors are subject to their portfolio’s value as of December 31st every year, it should be expected that investors would rush to the market to sell assets, driving down prices in an artificial manner in order to minimize tax liability.

Liquidity and Lookback Rules

Relatedly, liquidity is another important consideration for mark-to-market taxation. Just because an investor’s underlying assets appreciate in a given year does not mean that the investor has sufficient cash to pay any tax liability.

Senator Wyden’s proposal considers these two challenges and attempts to solve them by creating a so-called “lookback” charge rule for certain types of assets. For assets that are not easy to value and not easily sold, the investor’s tax is deferred until realization, but the tax is assessed for the entire length of ownership, as to eliminate any benefit of deferral.

Such a lookback rule has a number of shortcomings. First, as described in the working paper, the rule would be calculated for “nontradable property.” Defining a nontradable asset could be difficult. Presumably a stock or bond would be considered tradable, but what about the plethora of other financial instruments? A derivative is likely considered tradable, but what about derivatives without an over-the-counter market? A piece of art, for example, is tradable, but the market is likely quite shallow with limited comparable sales, making it unclear whether they should be taxed annually or subject to deferral. A definition related to “publicly traded” might be more comprehensible, though that is also ambiguous in some instances.

Assuming a reasonable definition of affected property is reached, other questions emerge from the proposal. While those with deferral-eligible property can delay their tax burden, others would not be able to. Because there isn’t a direct relationship between an increase in value and access to liquid capital, it is easy to imagine an investor whose stock ownership appreciates in a given year but lacks sufficient cash reserves to pay tax on the asset. Does this mean that the said investors with easily traded assets could be forced to liquidate at the end of the year to satisfy the tax burden? There could be many reasons that an investor in a tradable asset would not want to sell; ideally, a lookback rule would be broadened to allow the investor to decide when to liquidate the asset.

Second, ostensibly to reduce gaming the system and to compensate the government for delayed revenue, the proposal discusses assessing an interest charge or a surtax on investors that use the lookback period. However, this sort of structure would penalize entrepreneurs. Founders of new businesses, whose assets are untradeable business ownership, would be forced to pay a higher effective tax rate over the period of their investment than investors in more traditional assets, such as stocks and bonds. The proposal fixes one issue—gaming—by introducing another, penalizing risk taking.

Lookback rules also are difficult to create because of the uncertainty of future tax policy. As currently proposed, Senator Wyden’s approach would increase the capital gains tax rate to as high as 40.8 percent. But what if policymakers raise that tax rate in the future? Would investors receive the benefit of the lower rate during their lookback calculation for the years the rate was in effect or would they be subject to the new, higher rate for the entire lookback period? If the latter is adopted, the policy choice would further exacerbate the penalty on new business founders who delay paying the tax.

Without sufficiently overcoming these concerns, the mark-to-market approach could be quite harmful to the entrepreneurial community. Small businesses would face a difficult choice. They could defer their newfound tax obligations until they sell their business, resulting in increased interest charges and creating tax rate risk, or they can pay their newfound tax obligations annually, thus sacrificing cash flow at a time when most companies are cash-starved. In some instances, businesses might need to issue equity to raise sufficient capital, which would then dilute the entrepreneur's ownership stake.

It is also not clear how the lookback rules would work for investors who only surpass the thresholds for mark-to-market treatment for part of the time that they own the associated asset. Per Senator Wyden’s proposal, investors must meet an asset and/or income test to be subject to the new capital gains treatment. Presumably, some investors could be subject for some, but not all, years. If the policy does not account for such variance, the effective tax penalty for use of deferral increases, increasing the pressure on investors and entrepreneurs to liquidate holdings to satisfy the tax burden. Ideally, the lookback rule would account for such eligibility variance, but it makes the proposal even more complex.

Capital Losses

The flip side of asset appreciation is asset depreciation. Any mark-to-market system must adequately treat capital losses, allowing the individual to reduce their tax liability when assets decline in value. Allowing an individual to deduct all of their capital losses creates a symmetry; if gains are immediately taxable then losses should be immediately deductible. But allowing for immediate deductions for costs can be difficult, raising several important considerations.

First, immediate deduction for capital losses would fuel substantial volatility in federal tax receipts. Stock values tend to move similarly; the stock market increases for many at the same time, while declining at the same time at others. If one investor has a declining stock portfolio, it is quite likely that other investors have a similarly-performing portfolio. As the stock market declines, many investors would take advantage of deducting capital losses simultaneously. In many instances, the federal government would be providing refunds to wealthy investors as the stock market falls.

Other economic factors would be exerting pressure on the federal budget at the same time. During economic downturns, existing revenue sources decline: Individual income tax revenue falls as fewer individuals are employed full-time, and corporate tax revenue falls as fewer companies are profitable. Countercyclical spending programs, such as Medicaid, unemployment insurance, and other means-tested entitlements, further stretch the federal budget by increasing spending relative to prosperous years. Unlimited deductibility for losses would further expand the gap between revenues and spending, exacerbating volatility.

While this would be a dramatic new constraint on the federal budget, the federal government can run deficits. It would be much more difficult for state governments to handle such volatility. States use the federal tax code as the basis for their structures, meaning states would likely conform to any mark-to-market tax structure. States are less able to cope with revenue volatility due to their balanced budget requirements. All fifty states, either by practice or legal requirement, balance their budget annually, and states already struggle to manage their affairs during downturns. Adding further revenue uncertainty makes that problem even worse.

Additionally, unlimited loss deductions could give rise to “loss harvesting,” where investors purposely buy unprofitable investments in order to reduce their taxable income from other sources. For example, an investor with $2 million in taxable wage income could buy a failing business and use the losses from that business to reduce their taxable income over a series of years. This practice was widespread prior to the Tax Reform Act of 1986, which limited capital losses in any one year.

The tax law’s solution, however, leads to other problems. Currently, investors can only deduct $3,000 in capital losses per year. Additional losses must be carried forward to future tax years, but the undeducted losses are not adjusted for the time value of money, reducing their value. A $3,000 deduction in year one is significantly more valuable than a $3,000 deduction in year ten. By not allowing investors to adjust their carried forward balances penalizes investors and entrepreneurs.

An additional consideration is whether the individual can aggregate their losses. While it’s possible to design a mark-to-market system that is asset specific, it would be much better to assess tax based on the overall annual performance of the investor’s assets. For example, imagine an investor who owns two assets, stocks in ABC corp and XYZ corp. In one year, ABC gains $100, while XYZ loses $200. With full deductibility, that taxpayer would deduct $100 in losses. But imagine if they also owned a bond with a gain of $100. The gains and losses of the stock holdings should be available to offset the bond’s appreciation. Otherwise, the investor is taxed too much.

Ensuring losses are handled correctly is important. Under a mark-to-market system, these concerns become amplified as asset values are reviewed annually, not just at sale. It is much more likely that an investor would have losses over a single year than losses over the long-term. If Senator Wyden decides not to allow unlimited loss deductions each year, the proposal should allow investors to inflation-adjust residual losses in future years.

Exemptions

The proposal by Senator Wyden does not apply to all American investors. The Senator limits the mark-to-market approach to those with more than $1 million in income or more than $10 million in assets (or some combination of the two) for three consecutive years. Once an individual becomes an “applicable taxpayer,” the investor must use a mark-to-market approach for all of their assets.

These eligibility requirements create a large marginal rate cliff for taxpayers. Taxpayers have a large incentive to ensure their income stays below $1 million per year for three consecutive years to avoid triggering the provision. Similarly, there becomes an incentive for investors to potentially sell assets to avoid triggering the $10 million asset test.

The proposal also exempts $2 million in primary residences, $5 million in family farms, and $3 million in retirement assets from the $10 million asset test. Any assets owned above the stated exemption levels would be counted towards the $10 million asset test. For example, if an individual owns $5 million in retirement assets, $2 million would count towards their $10 million asset threshold.

While this approach spares many Americans from the burden of mark to market, it is still less than ideal as it increases complexity.

First, the exemption levels are not adjusted for marital status, creating a large marriage penalty within the tax code. A single investor or a married couple would be subject to the tax structure at the same level of income or assets, burdening married couples more than single filers.

Second, this structure injects more complexity into the taxation of investment income, particularly as it intersects with the current treatment of capital gains. For example, the proposal discusses a hypothetical mark-to-market taxpayer that purchases a home for $1 million. The home then appreciates to $3 million.

Under current law, the homeowner could exclude $250,000 or $500,000 of the gain from taxation, depending on their filing status, and would pay capital gains on the remainder. Under Senator Wyden’s proposal, this calculation becomes much more difficult. The $1 million in appreciation (bringing the home up to the $2 million threshold) would be subject to the existing $250,000 or $500,000 exclusion. The additional $1 million in appreciation would then be subject to the mark-to-market tax, via the lookback rule. The owner would pay the tax, plus some sort of likely interest or deferral charge, when the asset is sold. The calculation is cumbersome.

Providing exemptions ensures that not all investors are impacted by the policy, but it increases complexity within the tax code.

Inflation Adjustments

If the U.S. moved to a mark-to-market tax structure, allowing inflation adjustments for the cost basis of an asset becomes even more important to ensure that the investor’s tax basis more closely matches its underlying appreciation.

Currently, the U.S. tax code does not allow investors to adjust their cost basis for inflation. When the asset is sold and gains are realized, the investor must pay tax on the entire amount of appreciation. However, an asset’s gain is actually two components: the nominal increase due to inflation and the real gain due to actual increase in economic value. Taxing the nominal increase results in a tax on phantom gains, raising the after-tax cost of capital.

Ideally, any move to mark-to-market would be accompanied with a move to inflation adjustments of cost basis.[5]Without an adjustment, investors would be forced to pay taxes on both real and inflationary gains.

Other Items to Consider

Opportunity Zones

While Senator Wyden’s proposal asks for input on many of the items above, there are several other important considerations when drawing up specifics on a mark-to-market approach. First, the proposal should consider how it will interact with Opportunity Zones, a new tax incentive created by the Tax Cuts and Jobs Act. Investments in Opportunity Zones, via Qualified Opportunity Funds, provided three generous capital gains tax benefits. First, any investor that realizes capital gains and transfers the gains into a QOF can defer their initial capital gains liability. Second, if the QOF investment is held for at least five years, the cost basis of the QOF investment is stepped up to a higher amount. The basis is further adjusted after a seven-year holding period. Finally, if the QOF investment is held for more than 10 years, the investor’s QOF gain is completely tax free.

Opportunity Zones are, therefore, at direct opposition to Senator Wyden’s mark-to-market proposal. Now, Senator Wyden has been critical of Opportunity Zones in other contexts, so perhaps he would propose to eliminate the tax incentive, but the proposal does not address the interaction.

C Corporation Ownership

Further refinement is needed regarding the taxation of pass-through businesses as they relate to C corporation ownership. Wyden’s scheme envisions that mark-to-market would apply to pass-through businesses but not to C corporations. The proposal is correct to note that this could become a vehicle for avoiding the tax, but that risk must be weighed against the competing risk related to C corporation ownership of pass-throughs.

C corporations can, and sometimes do, own pass-through businesses for non-tax reasons. They use multiple organizations within their corporate umbrella to structure their affairs for legal, regulatory, or business use reasons. C corporations that own a pass-through as part of their corporate structure should not be unfairly targeted by this tax because of past structural decisions.

Conclusion

Mark-to-market tax systems do have a theoretical basis. In theory, taxing changes in net worth annually leads to a more accurate tax base, which captures income holistically. Implementation challenges regarding valuations, capital losses, liquidity, and exemptions, however, make it a difficult policy to design in practice. Balancing many competing demands without adding overwhelming complexity to the tax code is difficult enough with our current realization system, but near-impossible with a mark-to-market approach.

Even if a working tax structure is developed, it would still constitute a growth-damaging tax hike with particularly negative impacts on entrepreneurs. Senator Wyden should be applauded for tackling the difficult question of how to fund Social Security for the long-term, but a complicated $2 trillion tax increase is not the right approach.

[1]Senator Wyden is not the only legislator currently proposing a mark-to-market system. Senator Elizabeth Warren (D-MA) and others have supported the idea. Wyden’s, however, is the most detailed and the basis for this discussion.

[2]This paper will not discuss the economic impacts of Senator Wyden’s proposal, though they are significant. Mark-to-market taxation would raise tax rates on many Americans, reducing national income.

[3]The other commonly accepted definition of income is a consumption base that only includes an individual’s consumption. It does not include appreciation in the tax base, nor any saving done within the year, making it neutral to saving and investment.

[4]Senator Wyden has suggested in other places that the top income tax rate should increase above 37 percent, suggesting this rate could be higher for investors.

[5]Additionally, allowing inflation adjustments for the cost basis of an asset should be coupled with inflation adjustments for other tax provisions, such as interest deductions, to prevent tax avoidance.